Earlier this year, I went on the Dave Ramsey show to ask a question.

My husband and I want to upgrade his truck to something closer to his dream truck…with fewer miles than his current truck. We have also been dreaming about going back to Mexico for our 1 year anniversary. I knew we had the cash to pay for these things, but it seemed more extravagant than necessary.

After all, cheaper options exist…

I asked Dave, “After we are on Baby Step 6, how do we decide what is a reason able amount of money to spend on ‘fun stuff’?”

I explained that we are both 23, active duty military, and….on Baby Step 6.

(For those not familiar with Dave Ramsey’s baby steps, we are debt free except for our house, have a fully funded emergency fund of 3-6 months expenses, and are contributing a 15% into retirement.)

Dave answered my question: as long as we pay cash and keep up with our savings goals, we could absolutely have some fun, buy the truck, and go on vacation.

Ok cool. Thanks Dave! Now I have piece of mind.

After leaving the studio, I checked the YouTube live feed where the show was broadcast. The comments people left were downright nasty.

“Our taxpayer dollars are being wasted paying the military too much if they are already on Baby Step 6.”

“How can they be completely debt free at such a young age? Most of us are struggling just to get by.”

“Wow, that must be nice. She is YOUNG for Baby Step 6!”

So HOW, you ask, could we possibly be debt-free at age 23?

In all reality, we just listened to people who know more than us and avoided major financial mistakes. Let me dive into some of the things my husband and I have done (or not done) with our money…

1. Neither of us took out student loans.

My husband didn’t have any interest in college (and he still doesn’t, to be honest!). He joined the military right out of high school. Therefore, he didn’t take out any student loans. Pretty simple.

I’ma little bit different. I’m a total nerd who actually likes going to school. My parents didn’t have any money for me to attend college, so I had to innovate.

As a junior in high school, I was eligible for Post-Secondary Enrollment Option. This allowed me to attend local community college full-time (and the state government paid every penny).

I graduated from the community college with an Associate’s in Arts degree 2 weeks before I graduated high school.

I planned to pursue my bachelor’s degree, but withdrew from school just 2 weeks before class started because I didn’t get a full-ride scholarship. Student loans were not an option for me.

A few months later, I decided to join the military. After training, I used an awesome active duty benefit called Tuition Assistance to get my bachelor’s degree in Business Administration from Southern New Hampshire University. The military paid for every penny of this degree, but I had pay for books as I went. I continued working full-time on active duty while I earned my degree online.

I am about to start working on my master’s degree. Tuition Assistance and the GI Bill Top-Up program together will pay for my tuition.

So, neither of us had student loans…aka we didn’t have a huge hole of debt to pull ourselves out of before we started saving.

2. Neither of us bought things we couldn’t afford with credit cards. We save up for things and pay cash.

This was really hard. It still is.

Society tells us to want cool “things”. As our incomes started increasing, we naturally could afford bigger and better cars, a fancy house, and vacations. It is “easier” to eat out at a restaurant for dinner instead of cooking a meal at home. Things add up.

It is oh-so-easy to get approved for more and more credit nowadays. The temptation of “I can just put it on the card now and pay it off with my next paycheck” creeps up until, when you get your next paycheck, you realize the balance on your card is too much to pay off with this check.

This temptation is real, but it results in a roller-coaster that will spiral out of control.

I could see a train-wreck coming, so we nipped this in the butt before it got out of hand. We stopped using our credit cards completely for a while, until we knew our spending was completely under control. Now, we look at how much we have budgeted before we decided whether or not to buy something.

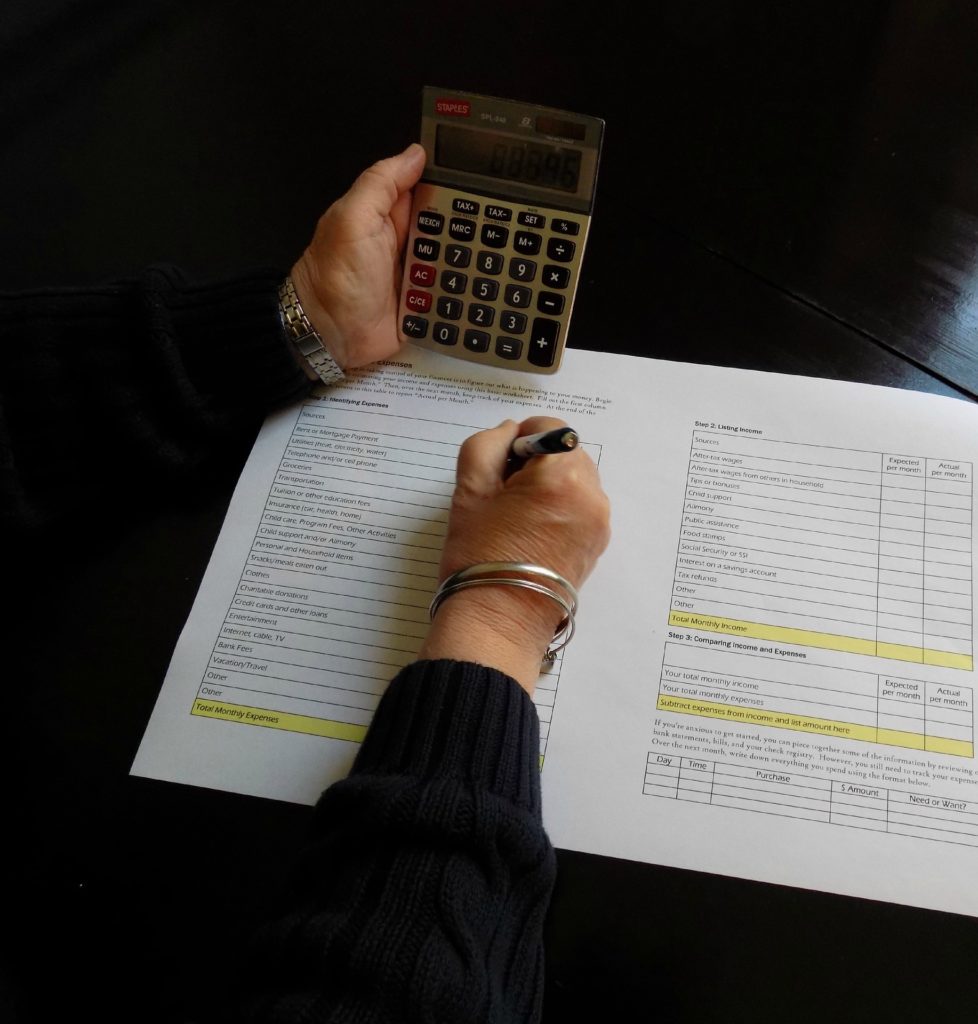

Developing our budget, we determine what a reasonable amount is in each category, spend no more than that, and save everything else.

Creating a zero-based budget was critical to our success.

When we find something we REALLY want, we save up for it. While saving for that item, we think about if having that item would really make our lives better, or if it would sit unused after a month or two. I am super anti-clutter, so if there’s a potential that we won’t use the item after it’s initial excitement wears off, we don’t buy it.

We now control our finances in such a way that we can integrate credit cards back into our financial picture as a way to earn travel rewards, but this is a very controlled process and we have the discipline to not overspend. Most importantly, we never pay a dollar of interest.

3. We bought reasonable vehicles, and quickly paid them off.

In the future, we will only be purchasing new vehicles with cash. The vehicles we currently own were bought on loans. After we saw how much it really sucks to pay the bank interest, we quickly paid our vehicles off and will continue to drive them as long as we can.

My husband has been dreaming about a new truck since before we got married, and his truck is really starting to get up there in mileage. We were planning to replace it this year, but since we decided to build a new house, his truck will be put on hold for another year or two.

My car is still running strong and has many miles left in it. We will save up to replace it just in case it quits, but I plan on driving it for several more years.

4. We live below our means and avoid comparing ourselves to others.

This can be really difficult too, especially when it seems like everyone around us is buying new stuff—all the time.

Our regular monthly expenses total about half our monthly income. The rest is used to save up for our current goal whether that be a new vehicle, down-payment for our next house, a vacation, or investing so we can retire early.

Now when we see others buying new stuff, instead of being jealous…we understand that most people probably bought that stuff on high-interest credit cards or a loan. They might be chained to those payments instead of buying their freedom.

5. We communicate about money.

My husband and I communicate on every aspect of our finances. He hates the “nerdy” stuff and can’t stand to look at a spreadsheet for more than 5 minutes, so he leaves the nerdy part to me.

However, he is aware of what our monthly budget is, where our money goes, and what our goals are. He understands the reason we only go out restaurants twice a month is so we have more money to free our future time. He can see everything in our monthly budget on YNAB and can input each transaction he makes so we can both see where our spending is at, in real-time.

We run the majority of our monthly expenses out of our joint account, but we also each have a personal account for a “fun-money” allowance every paycheck. This money can be spent however each of us sees fit, but when its gone, its gone. We don’t need to ask permission to spend money, but we usually talk to each other about what we want to purchase,especially if it is a larger item. We can spend our fun money as we get it on small things, or we can save it up for a bigger purchase.

Either way, it’s personal money to use as we see fit.

We never hide anything. We are open and honest about our purchases and allow each other to see into the other’s personal bank accounts.

It saddens me when we hear acquaintances talking about a big purchase they made but are hiding it from their spouse because they are afraid it will start a fight. Financial infidelity can ruin a marriage just as sexual infidelity would. If you feel the need to hide a purchase, then you probably shouldn’t have bought that thing–it isn’t in the best interest of your family.

If we can be debt-free this young, then you can too!

Avoid financial traps, follow a written budget, communicate with your spouse about your spending, and get on the same page about your financial goals.

Be sure to like my page on Facebook, follow me on Pinterest or Instagram to become part of the community.

Live Happy,

Alexis

- Nailing Your Marathon Hydration Strategy: A Comprehensive Guide

- Conquering Marathons in the Cold: A Comprehensive Guide

- Harnessing the Power of Technology for Successful Marathon Training

- Mastering the Marathon: The Ultimate Guide to Nutrition and Training

- Ultimate Guide to the Top 5 Running Shoes for Beginners in 2023

About Me: I’m Alexis, Founder of RunningMyBestLife! I am an avid recreational runner, half marathoner, wife, dog mom, busy professional, downhill skier in Northern Utah. My mission is to help new enthusiasts fall in love with the sport of running. I believe that running is a catalyst to taking control of your life and living your best life by design. Learn More –>

One of the most important things I’ve embraced in my adult life is, “What other people think about you is none of your business.” You’re doing all the right things and the haters are always going to be haters. Keep up the great work!

Thanks Jon, I totally agree! My husband and I will keep on doing what’s right for us and no one else’s opinion really matters. 😎